EU News Digest Latest News & Updates

EU News Digest Latest News & Updates

Investors like SoftBank have an obscure protection that will grant them hundreds of millions in shares if WeWork’s IPO value is lower than they bought in at in the private market.

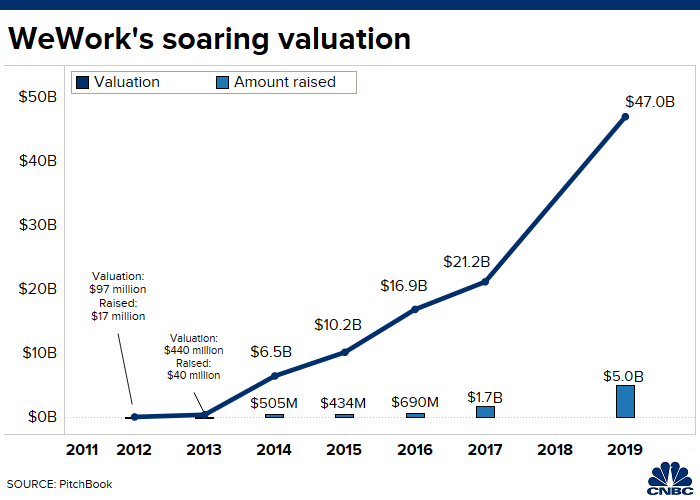

The fine print is known as a ratchet, and speaks to the opaque nature of private markets and sky-high valuations. The real estate start-up’s parent company was valued at $47 billion after its last funding round from SoftBank.

In the case of the WeWork’s parent company, it was a “partial ratchet” disclosed on page 115 of its S-1 filing. If the stock price comes in below a certain price in the IPO, investors like SoftBank will receive additional shares as compensation.

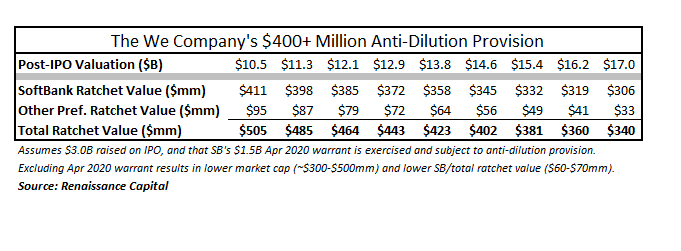

If triggered, these protections usually result in only a few million dollars worth of extra shares, according to Matthew Kennedy, senior IPO market strategist at Renaissance Capital. But because SoftBank’s latest round was so large and the possible down-round was looking to be less than half of that, the provision was expected to result in the world’s largest IPO ratchet.

“As a result, the founder and employees would see their own shares diluted,” Kennedy said. “It doesn’t look good for common shareholders to see that extra dilution on top of a down around.”

The provision could grant existing shareholders $200 million to $500 million worth of additional shares, most of which would go to SoftBank, Kennedy said. For example, if WeWork’s market cap came in at less than $14.5 billion post-IPO, the total value of additional shares issued to SoftBank under the provision would be more than $400 million.

These ratchet arrangements are not uncommon. It’s often seen as a win-win for late stage investors who might want a guarantee they won’t lose too much money. Late-stage Square investors were granted a full ratchet when it went public in 2014 that amounted in a $93 million in additional shares, according to Renaissance. A clause in Chegg’s IPO resulted in $146 million in additional shares, while Box issued $67 million worth of additional shares.

Aswath Damodaran, professor of finance at the Stern School of Business at New York University, said ratchets are often “glossed over” because they rarely kick in. The WeWork case is “unprecedented” since the venture capital valuation was so high. That “combination” makes it a “potentially dangerous situation,” he said.

“We really don’t know what these clauses are,” he said. “If I were a potential public market investor in WeWork, I would need complete disclosure on share count — tell me what’s going to happen after the offering.”

Damodaran, sometimes referred to as the “Dean of Valuation,” recently analyzed the company’s IPO filing and estimated that WeWork’s equity is worth $14 billion — about 70% below its latest private market valuation.

Opaque protections

The protection also speaks to how complicated these private market valuations can be. Damodaran highlighted that companies aren’t always required to explain what is baked into venture capital investors if things go south.

“Taking a VC investment and extrapolating the price of the company can be extremely dangerous — you have no idea what ratchet clauses were given,” he said. “The question you have to ask is ‘what protections did they get?’.”

After a series of setbacks in an initial public offering, WeWork is delaying the debut, a source told CNBC earlier in September. SoftBank’s billionaire founder Masayoshi Son is said to be in favor of removing Adam Neumann as WeWork’s CEO, people familiar with the matter told CNBC this week. SoftBank, WeWork’s largest investor, is also among those pushing to put the IPO on ice.

Damodaran said part of the reason for a delay is because the logistics of figuring out the share count after a ratchet would be “incredibly messy.”

“That’s why Softbank is putting pressure and saying don’t go public — this is a complete and total mess we’ll have on our hands,” he said. “This is going to be completely new ground if the IPO does happen.”

WeWork did not immediately respond to CNBC’s request for comment.

Until the company goes forward with a public offering, there are still missing details. Investors don’t know how many shares SoftBank and other investors get in the event this provision kicks in. If and when WeWork lists, they would be required to at least include a footnote that states how many new shares would be granted, Damodaran said.

The investor protections also change the script for bankers in WeWork’s eventual IPO roadshow. At this stage, Damodaran said Wall Street should demand to see the full agreement as a condition for investing in the company, and some may ultimately push for SoftBank to give up the provision altogether.

Even at $400 million in additional shares, SoftBank’s IPO provision would hardly make up for its total losses.

A WeWork stock market debut could force SoftBank to write down its multi billion-dollar investment if the company fetches an IPO valuation below $25 billion, Bernstein analysts said in a note earlier in September. That could lead to “large volatility” in SoftBank’s business in the near term, according to the firm.

“They’re taking a big loss — SoftBank has egg on its face right now,” Kennedy said. “That could cause more investors to be wary about investing in large unprofitable companies at sky high valuations.”