EU News Digest Latest News & Updates

EU News Digest Latest News & Updates

Hero Images | Hero Images | Getty Images

The year is ending but, with a little ambition, you can still find some opportunities to cut your 2019 tax bill.

The Tax Cuts and Jobs Act, which went into effect in 2018, did away with several breaks filers could take prior to the end of the year.

Miscellaneous itemized deductions — a grab-bag of breaks that includes the fees you’re paying tax preparer and your unreimbursed employee expenses— have been off the table since 2018.

Since the law roughly doubled the standard deduction ($12,200 for singles and $24,400 for married-filing jointly in 2019), other itemized deductions are out of reach for many filers.

Other write-offs have been limited as well: Consider there’s now a $10,000 cap on state and local tax deductions.

“Something to keep in mind is that we’re now in year two of tax reform and most of us are aware of how it affected us individually,” said Nathan Rigney, lead tax research analyst at H&R Block’s Tax Institute.

“We discovered we’re no longer itemizing,” he said.

Here are the tax breaks you can still nab as the year ticks down.

Ramp up savings

While you have until April 15, 2020 to make contributions to your individual retirement account and have them count for 2019, you have only until Dec. 31 to set aside money in your 401(k) plan at work.

This year, you can save up to $19,000, plus an additional $6,000 if you’re age 50 and over.

Contributions that generally come out of your paycheck are made pretax and they reduce your taxable income for the year.

Here’s a sweetener: If you’re in a high-deductible health plan at work and have a health savings account, set aside a few more dollars there.

You can contribute up to $3,500 in 2019 if you have self-only coverage or $7,000 for family plans.

HSAs have three key tax benefits: Contributions are made pretax or are tax-deductible, and they accumulate without taxes. You can make withdrawals free of taxes to cover qualified medical expenses.

And here’s a fourth: Your HSA contribution at work avoids Social Security and Medicare taxes. This levy is 15.3% and you share it with your employer.

Be environmentally friendly

EXTREME-PHOTOGRAPHER | E+ | Getty Images

This year, it pays to be green.

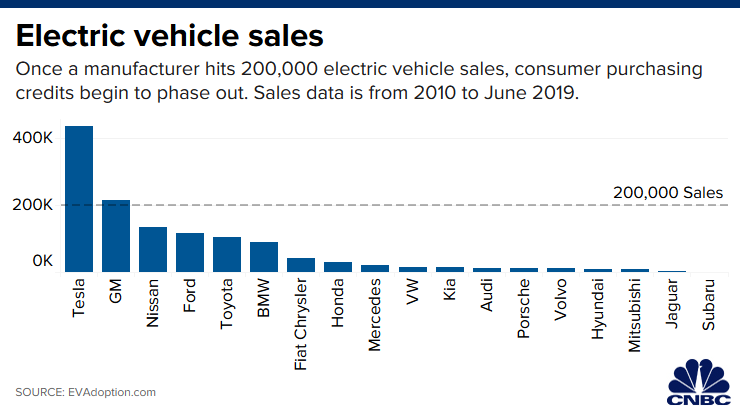

The federal electric vehicle tax credit offers up to $7,500 per new auto purchase.

Pay close attention to the number of units sold: The amount of the credit begins to phase out for a manufacturer after more than 200,000 cars are sold.

Meanwhile, if you’re thinking about getting solar panels, you can nab a 30% credit for buying and installing them this year.

Next year, the value of the credit declines to 26%, and then to 22% in 2021. After that year, homeowners lose the tax break altogether.

Get an education

skynesher | E+ | Getty Images

Hit the books and claim the lifetime learning tax credit, which is worth up to $2,000 per return.

“Pay for your expenses by Dec. 31, even if you take the classes in the first quarter of next year,” said Lisa Greene-Lewis, CPA and tax expert at TurboTax. This credit is applicable to all years of post-secondary education and for courses at an eligible educational institution to help with your job skills.

How much you can claim is based on your income. The credit phases out for single filers with modified adjusted gross income between $58,000 and $68,000 in 2019 ($116,000 to $136,000 for married couples filing jointly).

Don’t forget: If you’re also paying off a student loan, you can take a deduction for the interest of up to $2,500. This is an above-the-line deduction, so you don’t have to itemize your return to get it.

Medical expenses

Hero Images | Hero Images | Getty Images

If you’re already itemizing — that is, your total itemized deductions exceed the standard deduction of $12,200 for singles ($24,400 for married couples) — you might be eligible to claim qualified medical expenses.

In this case, you can only deduct the expenses to the extent they exceed 10% of your adjusted gross income in 2019 (that’s up from 7.5% in 2018).

Not taking itemized deductions this year? Consider tapping your health-care flexible spending account — a tax-advantaged account whose balance you must use or lose each year — to cover qualified medical costs.

Unlike an HSA, you don’t need to be in a high-deductible plan at work to qualify for an FSA.

Charitable donations

Here’s a win-win: You donate to your favorite charity and you pick up a deduction for doing so.

Juice up your deduction by “bunching” multiple years’ worth of donations into one year so that you can itemize on your federal tax return.

Give wisely. While cash is the fastest way to donate, a direct transfer of appreciated investments is the most tax-savvy way to give.

More from Personal Finance:

How to avoid ‘porch pirates’ this season

Nearly 80% of employers think workers’ finances are out of whack

Medicare would cover dental and vision — if Senate OKs this bill

This way, you avoid recognizing the gain from cashing out those appreciated stocks, and you can write-off the fair market value of the investments.

Save all of your acknowledgement letters from the charities. You’ll need them at tax time.

“You need to keep track of the tax receipts and substantiate the amount you’re giving when you take deductions,” said Tony Oommen, vice president and charitable planning consultant at Fidelity Charitable.

Don’t count on these deductions coming back

This year, Congress chose not to renew a basket of tax breaks that expired in 2017 and 2018.

These so-called tax extenders are a package of temporary provisions in the code that must be cleared by Congress retroactively each year in order for filers to claim them.

They include a $4,000 above-the-line deduction for college tuition and fees, a deduction for mortgage interest premiums and an exclusion of canceled debt in the event your home is foreclosed.

Though taxpayers are watching to see if Congress might push through a tax package for year-end, don’t bet your 2019 tax return on it.

“We haven’t seen any tax extenders packages pass through Congress,” said Rigney of H&R Block. “Something to keep an eye on is any language in the budget bill that’s due on Dec. 20. But don’t rely on any speculation.”